Why are the Experts Pessimistic About the Future of Homeownership?

Insight Video Preview

The national homeownership rate has been declining for over a decade. According to the experts, we can expect further declines.

The homeownership rate peaked at 69.2 percent in the last half of 2004, in the middle of the housing boom. The rate fell 1.4 percentage points during the last gasp of the boom, just prior to the onset of the Great Recession. During the recession, the foreclosure crisis reduced the homeownership rate a further 3.1 percentage points. And in the seven years since the end of the Great Recession, instead of bouncing back, the homeownership rate has dropped an additional 4.5 percentage points to less than 63 percent today, the lowest rate in half a century.

This decline in the homeownership rate has triggered debate among housing experts, especially among those who view broad access to homeownership as a signature achievement of American economic policy. Of particular concern is the pronounced drop in the homeownership rate in demographic groups that historically have had lower-than-average homeownership rates. For instance, the homeownership rate among African Americans spiked briefly during the housing boom, rising from a low of 41.2 percent in Q3 1995 to a high of 49.7 percent in Q2 2004. Since then, African Americans have given back virtually all those gains; their homeownership rate has fallen eight percentage points to 41.7 percent, the lowest rate among the racial/ethnic groups tracked by the Census Bureau.

If the experts are right, the homeownership rate will decline even further in future decades. Homeownership rates below 60 percent are not out of the question according to these projections. How likely are these projections to come to fruition? What factors lead the experts to this conclusion? And, just as important, who will own a home? Will historically underserved groups recover the ground lost during the last decade, or are they likely to be stuck indefinitely at substantially lower rates of homeownership than the population as a whole?

The history of homeownership

For most of the first half of the 20th century, the homeownership rate in the U.S. varied between 44 and 48 percent (Exhibit 2). The return of military personnel from World War II combined with availability of low-interest mortgage benefits provided by the G.I. Bill triggered a surge in the homeownership rate, which jumped to 55.0 percent by 1950. The institutionalization of the 30-year fixed rate mortgage and public policy initiatives such as the creation of FHA, VA, and the GSEs provided additional support for homeownership. The homeownership rate reached 61.9 percent in 1960, then continued to climb, albeit more slowly, until it reached its peak of just under 70 percent in 2004.

How to forecast homeownership

All forecasts rely on the future looking a lot like the past in important ways. Projecting the future homeownership rate is no exception. For homeownership, projections rely primarily on historical differences in the homeownership rate across age and demographic groups. By interacting those observed differences in homeownership with Census projections of the growth of the population in each age and demographic group, we can calculate a reasonable approximation of the future overall homeownership rate.

The homeownership rate increases with the age of a group (Exhibit 3). The increase is rapid in early years as people marry, start families, and advance in their careers. The homeownership rate continues to increase after age 35 but at a much slower pace.

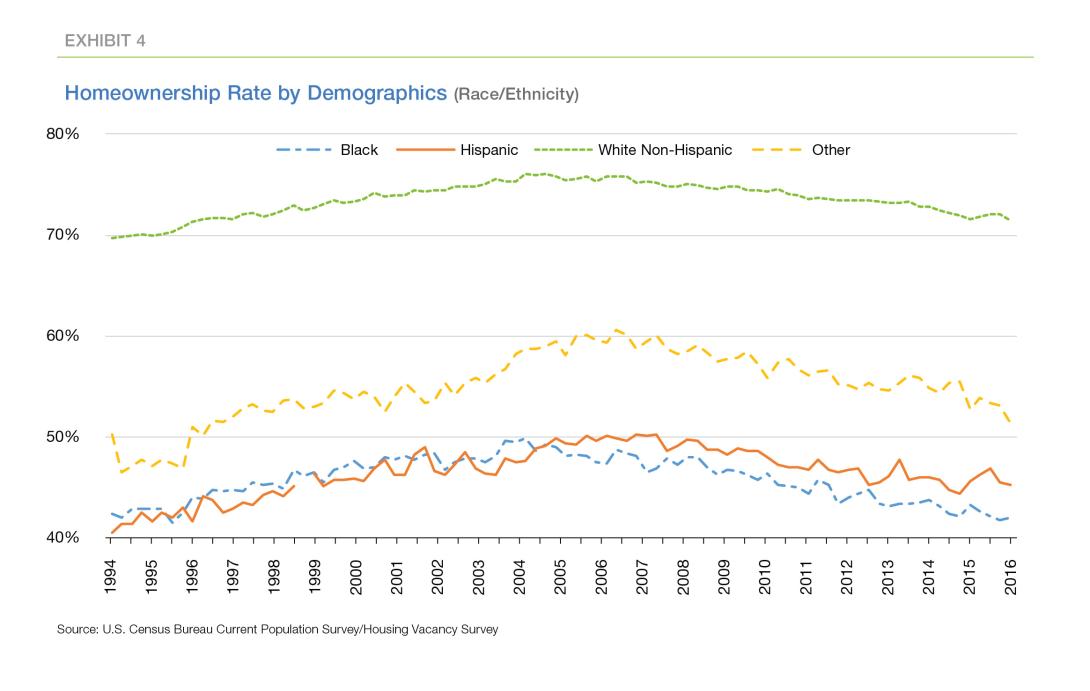

Historically, white, non-Hispanic households (Whites) have recorded the highest rates of homeownership. African-Americans (Blacks), Asians, and Hispanics typically have had homeownership rates 18 to 28 percentage points lower than Whites (Exhibit 4). These differences persist even after accounting for differences in income and education.

If the differences in homeownership between different age and demographic groups never changed, future homeownership rates could be projected very accurately. After all, at any point in time, the homeownership rate for the U.S. as a whole is just the weighted average of the homeownership rates in each of the age/demographic groups. By tracking the projected growth of each age/demographic group, that weighted average can be calculated for every future year.1

Of course, it's not that simple. Age- and demographic-specific differences in homeownership rates are not immutable. For instance, Exhibit 5 compares the relationship between age and homeownership in 2015 to the relationship in 1990.

Those in their early 30s in 1990 had a higher homeownership rate than Millennials in their early 30s do today. That reduction in the homeownership rate of people in their early 30s might be due to the higher student debt burden of the Millennials. Or it might be due to tighter credit availability, higher house prices relative to household income, and changes in the public policies designed to assist first-time homebuyers. Alternatively, it might reflect a generational shift in the appeal of homeownership, due, perhaps, in part to the experience of the mid-2000s housing collapse. Most likely, the difference in the homeownership rate reflects some mixture of all of the above influences.

Why the experts disagree

Factors like those described in the paragraph above account for much of the uncertainty in projecting the future homeownership rate. Changes in the housing and mortgage industries, changes in public policy, changes in social attitudes, and macroeconomic shocks such as the Great Recession—all these and more may alter the future. Twenty years in the future, today's Millennial 35-year-olds will not act exactly like today's Baby Boomer 55-year-olds. Or perhaps they will. And this is where experts begin to part ways.

Exhibit 6 illustrates this issue. In 1990, the 35-to-39 year-olds had a homeownership rate of 63 percent. Today the homeownership rate among the same group, which are now 60-to-64 years old, is 76 percent, 13 percentage points higher than 25 years ago.

Now consider today's Millennials between 35 and 39 years of age. Their current homeownership rate is 55 percent, eight percentage points lower than the 35-to-39 year-olds' rate 25 years previously. Does this lower rate among today's 35-to-39 year-olds reflect a permanently different generational attitude toward homeownership? If so, then perhaps the homeownership rate 20 years from now among these Millennials may be around 68 percent—13 percentage points higher than it is today (reflecting the impact of aging) but 8 percentage points lower than the rate among today's 60-to-64 year-olds (reflecting the different preferences/behaviors of the Millennial and Baby Boomer generations). But what if the lower homeownership rate of the Millennials is a transitory difference, the slowly-decaying effect, say, of the Great Recession? Then 20 years from now, the homeownership rate of these Millennials may be about 76 percent, the same as today's Baby Boomers.

Experts have argued for different answers to this question—whether observed shifts in age-specific homeownership rates are permanent or temporary—and, as a result, have come up with different projections of the future homeownership rate. The Joint Center for Housing Studies (JCHS), a pioneer in this methodology for analyzing homeownership, assumes for the most part that recent shifts are temporary and that today's 35-year-olds will resemble today's 60-year-olds in 25 years. The Urban Institute (UI) has adopted the opposite approach. They assume that shifts like the reduction in the homeownership rate of 35-year-old Millennials reflect a generational difference that will persist as these Millennials continue through life.2

Other Views

The Joint Center for Housing Studies (JCHS) and Urban Institute (UI) are not the only experts predicting future homeownership rates, and the range of professional opinion is much wider than is suggested by Exhibit 7. Last spring, the American Real Estate and Urban Economic Association hosted a symposium where seven experts debated the possibility that the homeownership rate could fall by as much as 20 percentage points by 2050. The papers from that symposium were published in CityScape and summarized by us in a previous article. And last year, the Mortgage Bankers Association proposed a more optimistic view of future homeownership rates. While the MBA's conclusions are on the high end of professional opinion, they are carefully reasoned and highlight the difficulty of projecting future homeownership.

Nonetheless, the JCHS and UI are recognized as the pioneers and leading experts on this question. We chose to focus on their approaches to emphasize the central role played by increasing diversity in projecting future homeownership rates and to question the critical assumption that the historical gaps in homeownership rates between demographic groups either cannot or will not be narrowed in future decades.

What do the experts predict?

Exhibit 7 below compares two long-term projections of the homeownership rate. The solid line represents the JCHS approach, that is, it assumes that 20 years from now today's 35-year-olds will behave like today's 55-year-olds. The dashed line represents the UI approach, that is, generational differences are assumed to persist over time.3

The JCHS approach projects the homeownership rate to remain around 63 percent over the next 10 years. After 2024, the homeownership rate falls steadily and drops to 62 percent by 2054. The UI approach projects an immediate and much more severe drop in the homeownership rate. By 2044, the UI approach projects the homeownership rate will fall below 60 percent.

The shape of both of these projections—a relatively stable homeownership rate for a decade followed by a steady decline—represents the conflicting influences of an aging population but a more diverse one.

Homeownership increases with age, and the coming years will see an older America. For example, the Census Bureau projects the share of the population over 65 will increase from 15 percent today to 19 percent in 2025. The larger share of older Americans accounts for the near-term stabilization in the projected homeownership rate.

Counterbalancing the influence of aging is the projected increase in demographic diversity in the U.S. Non-Hispanic whites comprise 73 percent of the Baby Boom generation. In contrast, Millennials are much more diverse—only 59 percent of Millennials are non-Hispanic whites. As the Baby Boom generation inevitably leaves the stage, the future America will come to look more like the diverse Millennials than the white-dominant Baby Boomers. If historical demographic differences in homeownership rates persist, this increased diversity eventually will produce a lower homeownership rate.

The UI approach projects a homeownership future similar in shape, but significantly lower in level, than the JCHS approach. This difference reflects the lower homeownership rate of Millennials compared to the rates of Gen Xers and Baby Boomers when they were the age of today's Millennials. The UI approach assumes that this difference represents a permanent characteristic of the Millennials rather than a temporary deviation from historical norms. As a result, the UI approach incorporates a more pessimistic view of the future homeownership rate than the JCHS approach. By 2044, the UI approach projects a homeownership rate three percentage points lower than that projected by the JCHS approach.

Demographic differences

Both the JCHS and UI approaches assume that demographic differences in homeownership will persist. Exhibit 7 displays projected homeownership rates of 35-year-olds in four demographic groups. In both approaches, the gaps between white and non-white homeownership rates are not projected to narrow.

Is this future inevitable?

Whether we favor the JCHS or UI approach to projecting future homeownership rates, both projections have troubling aspects. The homeownership rate is expected to grind lower, and demographic differences in homeownership appear to be ineradicable. Contemplating this future, we are reminded of Scrooge's question: "Are these the shadows of the things that Will be, or are they the shadows of the things that May be only?"

We believe these projections may be overly pessimistic. To begin, consider Exhibit 9 which displays two different projections of future homeownership rates. Both projections use the JCHS approach, but the projections are calculated using different starting points. The higher, solid line represents a projection based on the Census data available only through the year 20004. The lower, dashed line represents the same methodology applied to Census information through 2014. The earlier data suggested the homeownership rate in 2014 would be almost 66 percent, when, in fact, it turned out to be more than three percentage points lower. The gap between the two projections narrows a bit over time but still exceeds two percentage points as late as 2054.

Admittedly, the years since 2000 have witnessed turbulence in the housing market of a magnitude that virtually no one foresaw. But that's the point. Both the JCHS and UI approaches project future homeownership rates by, in essence, applying some fancy arithmetic to current conditions. These approaches do not—nor do they claim to—incorporate future macroeconomic disruptions, significant policy changes, or shifts in social attitudes in their calculations. These types of influences ultimately will determine how accurate or off-target the JCHS and UI projections are.

And what types of unforeseen influences might arise? We can think of three, and we're sure there are many more we're overlooking.

- First, the future of housing finance has yet to be sorted out. The GSEs are in their eighth year of conservatorship—a tenure that was not foreseen by anyone when they entered conservatorship in September 2008. No one knows when a consensus on the complex issues surrounding housing finance will be reached in Congress, but whatever choices are made will surely influence the future path of homeownership.

- Second, Millennials may finally commence to marry, start families, and buy homes at the faster pace posted by previous generations. This catch-up has been predicted many times by many analysts. Perhaps it will actually occur.

- Third, the factors accounting for the lower homeownership rates of non-white demographic groups may be overcome.

- The income and education gaps that are responsible for some of the differences may be narrowed or eliminated as the U.S. becomes a "majority minority" country.

The residual gaps—the ones that can't be explained by income or education and that highlight constraints on access to credit—may be erased at last. Today's mortgage finance system is designed for mass production to reduce costs. It works best for borrowers who are easily tracked and evaluated, borrowers with readily-measured and scored credit performance, with long-standing bank and credit accounts, and with significant tangible assets. The machinery of underwriting, approving, servicing, and risk-managing mortgages is honed to seek out this type of customer.

Some creditworthy borrowers don't fall into this easily evaluated category. Evidence of their good credit performance—evidence such as a long record of on-time rental payments—may be more difficult or expensive to gather. Some of these borrowers may come from multigenerational households where the economic resources of the entire household can be tapped if needed to make mortgage payments.

As the population becomes more diverse, borrowers that don't fit smoothly into today's mass production mortgage industry will come to comprise a larger and larger share of the potential market More potential home buyers may live in multi-generational households. More potential home buyers will have credit histories that cannot easily be traced by today's methods. And as these types of potential home buyers comprise a larger and larger share of the population, it will become increasingly expensive to overlook them. Profit-oriented financial institutions will be motivated to find better ways to serve them.

To be sure, the projections of the JCHS and UI approaches provide a useful starting point for the discussion of the future of homeownership. They help us quantify "the things that May be only" if current patterns of behavior are unchanged. However, the points listed above remind us that the actual future will be determined by a combination of industry evolution, unforeseen economic shocks, societal shifts, and the difficult policy choices that our nation has yet to make.

Appendix: Data and methodology for the projections

We used data collected by the Integrated Public Use Microdata Series (IPUMS-USA)5 from the 2000 Census, 2010 American Community Survey (ACS)6 and 2014 ACS. The microdata allows us to tabulate homeownership rates by age and race/ethnicity of householder7.

We partition the entire non-institutional population into categories corresponding to the race/ethnicity of the individual and household. We construct age categories grouped in 10-year increments from 15 to 85 (i.e. 15-24 year-olds, 25-34 year-olds, … ,74-84 year-olds and 85+) and race/ethnicity categories corresponding to Hispanic, White non-Hispanic, Black non-Hispanic, and Other. We compute the headship and homeownership rate for each unique group for each of the three years (2000, 2010 and 2014).

JCHS Approach

What we call the JCHS approach calculates the group average headship and homeownership rates in 2014 and applies those averages throughout the projection period. The headship and homeownership rates are then combined with Census population projections to compute total households and homeownership rates for 10-year periods from 2014 to 2054.

We multiply the estimated headship rate for each age and race/ethnicity group by the projected population for that group to get an estimate for the number of households. We then multiply the estimated number of households by the homeownership rate to get the age and race/ethnicity group number of homeowner households. The aggregate homeownership rate is then calculated by taking the ratio of the total sum of homeowner households to the total sum of households.

UI Approach

The UI approach follows in the spirit of the UI's household and homeownership projections, with some simplifications for exposition. First, we compute the 10-year difference in headship and homeownership rates by cohort from 2000 to 2010. For example, we compare the headship and homeownership rates for 25-34 year-olds in 2010 to the headship and homeownership rates for the same race/ethnic groups at ages 15-24 in 2000. The differences are then applied in 10-year increments going forward. New cohorts are assumed to enter at ages 15-24 with the observed 2014 average headship and homeownership rate for 15-24 year-olds.

Using the estimated age and race/ethnicity headship and homeownership rates we compute the aggregate homeownership rate as in the JCHS approach.

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP

Sean Becketti, Chief Economist

Len Kiefer, Deputy Chief Economist

Footnotes

- However, as long as the future growth rates of each age/demographic group remained uncertain, homeownership rates could not be forecast perfectly.

- This description oversimplifies the JCHS and UI analyses in order to highlight an essential difference between the approaches. For a detailed description of each approach, see JCHS Baseline Household Projections for the Next Decade and Beyond March 2014 and UI Headship and Homeownership: What Does the Future Hold? June 2015

- The projections in Exhibit 7 represent our own calculations using the [data sources & Census projections]. The "JCHS approach" incorporates the assumption that the homeownership rates in each age/demographic group remain at today's levels. The "UI approach" incorporates the assumption that generational differences are permanent. Neither the Joint Center for Housing Studies nor the Urban Institute have reviewed or approved these illustrative examples. As noted above, the actual JCHS and UI approaches involve additional complexities.

- Both homeownership rate projections use the same population projections from Census but differ in the homeownership and household headship assumptions for different age and race/ethnicity groups.

- IPUMS-USA, University of Minnesota, www.ipums.org.

- Homeownership rates for the ACS are close to those observed in the Decennial Census.

- The householder is the primary respondent to the survey. For household level statistics like the homeownership rate we classify each household based on the characteristics of the primary respondent. For person-level statistics, like the headship rate, we use individual level characteristics.

- The Census population projections are based on total resident population, but our analysis focuses on the Non-institutional population. We took the growth factors in resident population from the Census projections and applied them to the 2014 ACS age population counts. In effect, we’re assuming the age/race-specific rate of institutionalization remains unchanged throughout the projection period.